Next: About this document ...

Up: Poisson Process, Spike Train

Previous: Poisson Process, Spike Train

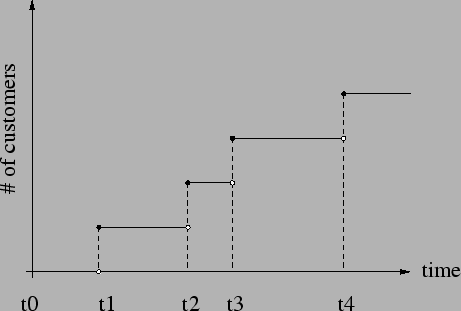

Figure 1:

Counting process

|

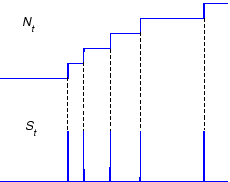

Let Fig. 1 be a graph of the customers who are entering a bank.

Every time a customer comes, the counter is increased by one. The time of the

arrival of

th customer is

th customer is  . Since the customers are coming at

random, the sequence

. Since the customers are coming at

random, the sequence

, denoted shortly

by

, denoted shortly

by

, is a random sequence. Also, the number of customers

who came in the interval

, is a random sequence. Also, the number of customers

who came in the interval ![$ (t_0, t]$](img6.png) is a random variable

(process). Such a process is right continuous, as indicated by the graph in

Fig. 1.

is a random variable

(process). Such a process is right continuous, as indicated by the graph in

Fig. 1.

As it is often case in the theory of stochastic processes, we assume that

the index set, i.e. the set where

is taking values

from, is

. Therefore, we have a sequence of non-negative random

variables

. Therefore, we have a sequence of non-negative random

variables

as

WLOG1 let  and

and

, then

is called a point process (counting process), and is denoted shortly by

, then

is called a point process (counting process), and is denoted shortly by

.

.

Let

be inter-arrival time, then the sequence of

inter-arrival times

be inter-arrival time, then the sequence of

inter-arrival times

is another stochastic process.

is another stochastic process.

Special case is when

is a sequence of

i.i.d.2 random

variables, then the

sequence  is called a renewal process.

is the associated renewal point process, sometimes also

called renewal process. Also, keep in mind that

is called a renewal process.

is the associated renewal point process, sometimes also

called renewal process. Also, keep in mind that

.

.

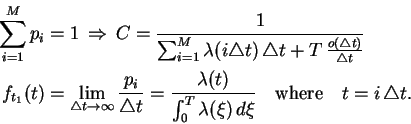

Definition (Poisson process) A point process

is

called a Poisson process if and  satisfies the following

conditions

satisfies the following

conditions

- its increments are stationary and its non-overlapping increments are

independent

-

-

Remarks

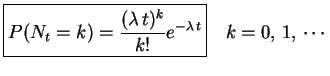

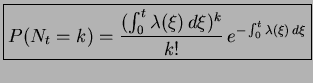

Theorem Let

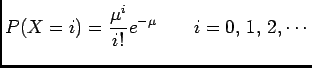

be a Poisson process, then

|

(1) |

The expression on the left hand side of (1) represents the

probability of  arrivals in the interval

arrivals in the interval ![$ (0, t]$](img34.png) .

.

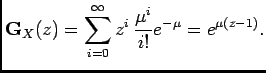

Proof A generating function of a discrete random variable  is

defined

via the following z-transform (recall that the moment generating function of a

continuous random variable is defined through Laplace transform):

is

defined

via the following z-transform (recall that the moment generating function of a

continuous random variable is defined through Laplace transform):

where

. Let us assume that is a Poisson random variable with

parameter

. Let us assume that is a Poisson random variable with

parameter  , then

and

, then

and

|

(2) |

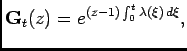

Going back to Poisson process, define the generating function as

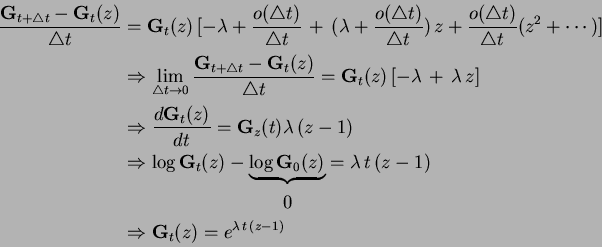

Then we can write

Furthermore

Comparing this result to (2) we conclude that  is a Poisson

random variable with parameter

is a Poisson

random variable with parameter

.

.

Theorem If

is a Poisson process and

is the inter-arrival time between the

is the inter-arrival time between the

th and

th and

th events, then

is a sequence of i.i.d. random variables with exponential

distribution, with parameter

th events, then

is a sequence of i.i.d. random variables with exponential

distribution, with parameter  .

.

Proof

exponential

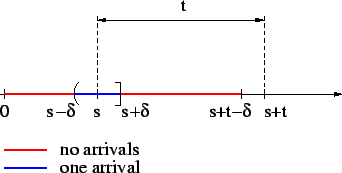

Figure 2:

Event description

|

Need to show that  and

and  are independent and is also

exponential.

are independent and is also

exponential.

![$\displaystyle P(T_2>t \vert T_1\in(s-\delta, s+\delta])= \frac{P(T_2>t, T_1\in(s-\delta, s+\delta])}{P(T_1\in(s-\delta, s+\delta])}$](img54.png) |

(3) |

The event

![$ \{T_2>t, T_1\in(s-\delta, s+\delta]\}$](img55.png) is a subset of the event

described by Fig. 2, i.e.

no arrivals one arrival no arrivals

is a subset of the event

described by Fig. 2, i.e.

no arrivals one arrival no arrivals

From (3)

![$\displaystyle P(T_2>t \vert T_1\in(s-\delta, s+\delta]) \le e^{-\lambda (t-2 \delta)}$](img59.png) |

(4) |

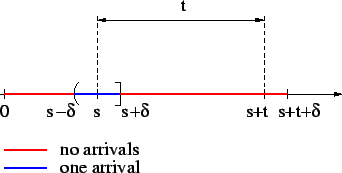

Similarly, the event described by Fig. 3 is a subset of

the event

, therefore

From (3)

![$\displaystyle P(T_2>t \vert T_1\in(s-\delta, s+\delta]) \ge e^{-\lambda t}$](img61.png) |

(5) |

Figure 3:

Event description

|

From (4) and (5), using squeeze theorem

, it follows

Therefore, is independent of , and is exponentially

distributed random variable.

, it follows

Therefore, is independent of , and is exponentially

distributed random variable.

Theorem

-

![$ E[N_t]=\lambda t$](img65.png)

-

![$ Var[N_t]=\lambda t$](img66.png)

Proof

Recall that

![$ \mathbf{G}_t(z)=E[z^{N_t}]$](img67.png) , then

, then

Likewise

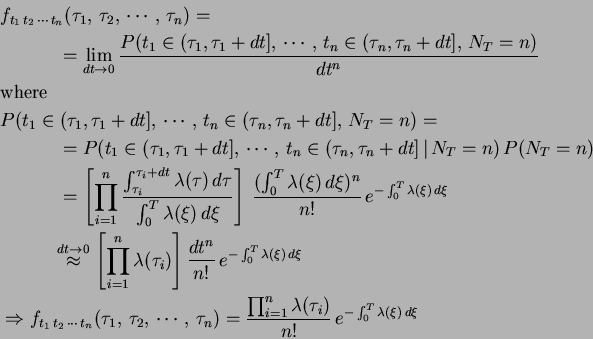

Theorem (Conditioning on the number of arrivals) Given that in the

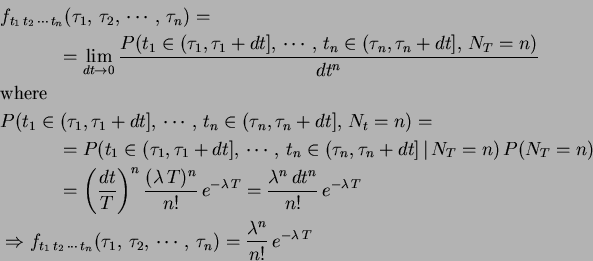

interval ![$ (0, T]$](img70.png) the number of arrivals is

the number of arrivals is  , the

, the  arrival times

are independent and uniformly distributed on

arrival times

are independent and uniformly distributed on ![$ [0, T]$](img73.png) .

.

Proof

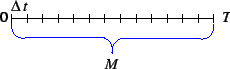

Figure 4:

Uniform bins

|

Independence of arrival times  ,

,  etc. directly follows from

independence of non-overlapping increments. In particular let and

be arrival times of first and second event, then

etc. directly follows from

independence of non-overlapping increments. In particular let and

be arrival times of first and second event, then

Suppose that we know exactly one event happened in the interval ,

and suppose the interval is partitioned into  segments of length

segments of length

, as shown in Fig. 1. Let

, as shown in Fig. 1. Let  be the probability of

event happening in the

th bin, then

be the probability of

event happening in the

th bin, then

. From the

definition of Poisson process it follows that

. From the

definition of Poisson process it follows that

, say

, say

. The

constant

. The

constant  is determined from

is determined from

Let be a random variable corresponding to the time of arrival, then

the probability density function (pdf) of can be defined as

where where |

|

Therefore, is uniformly distributed on .

Let and be the arrival times of two events, and we know exactly two

events happened on . Also assume that and represent mere

labels of events, not necessarily their order. Given that happened in

th bin, the

probability of occurring in any bin of size

is proportional

to the size of that bin, i.e.

, except for

the

th bin, where

th bin, the

probability of occurring in any bin of size

is proportional

to the size of that bin, i.e.

, except for

the

th bin, where

. By rendering the bin

size infinitesimal, we notice that the probability remains constant over

all but one bin, the bin in which occurred, where

. By rendering the bin

size infinitesimal, we notice that the probability remains constant over

all but one bin, the bin in which occurred, where  . But this set

is a set of measure zero, so the cumulative sum over again gives

rise to uniform distribution on .

. But this set

is a set of measure zero, so the cumulative sum over again gives

rise to uniform distribution on .

Question

What is the probability of observing events at instances

on the interval ?

on the interval ?

Since arrival times

are continuous random variables,

the answer is 0. However, we can calculate the associated pdf as

are continuous random variables,

the answer is 0. However, we can calculate the associated pdf as

Question What is the power spectrum of Poisson process?

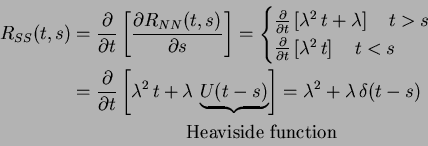

It does not make sense to talk about the power spectrum of Poisson process,

since it is not a stationary process.

In particular the mean of Poisson process is

and its autocorrelation

function is

Since

, we conclude that

is

not stationary (in weak sense), therefore it does not make sense to talk about

its power spectrum. Let us define the following stochastic process

(Fig. 5)

, we conclude that

is

not stationary (in weak sense), therefore it does not make sense to talk about

its power spectrum. Let us define the following stochastic process

(Fig. 5)

spike train spike train |

(6) |

Figure 5:

Spike train

|

The fundamental lemma says that if

, where

, where  is a linear

operator, then

is a linear

operator, then

Since differentiation is a linear operator we have

Also, it can be shown using theory of linear operators that

Thus,  is WWS3

stochastic process, and it makes sense to define the power spectrum of such a

process as a Fourier transform of its autocorrelation function i.e.

is WWS3

stochastic process, and it makes sense to define the power spectrum of such a

process as a Fourier transform of its autocorrelation function i.e.

Therefore, the spike train

of independent times

behaves almost as a white noise, since its power spectrum is flat

for all frequencies, except for the spike at

of independent times

behaves almost as a white noise, since its power spectrum is flat

for all frequencies, except for the spike at  . The process

defined by (6) is

a simple version of what is in engineering literature known as a

shot noise.

. The process

defined by (6) is

a simple version of what is in engineering literature known as a

shot noise.

Definition (Inhomogeneous Poisson process) A Poisson process with a

non-constant rate

is called inhomogeneous Poisson process.

In this case we have

is called inhomogeneous Poisson process.

In this case we have

- non-overlapping increments are independent (the stationarity is lost though).

-

-

Theorem If

is a Poisson process with the rate

is a Poisson process with the rate

, then is a Poisson random variable with parameter

, then is a Poisson random variable with parameter

i.e.

i.e.

|

(7) |

Proof The proof of this theorem is identical to that of

homogeneous case except that

is replaced by

. In particular,

one can easily get

|

(8) |

from which (7) readily follows.

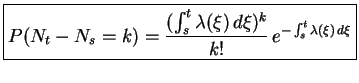

Theorem Let

be an inhomogeneous Poisson process with the

rate

and let  , then

, then

|

(9) |

The application of this theorem stems from the fact that we cannot use

, since the increments are no longer stationary.

, since the increments are no longer stationary.

Proof

Thus,  is a Poisson random variable with parameter

is a Poisson random variable with parameter

, and (9) easily follows.

, and (9) easily follows.

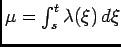

Theorem

-

![$ E[N_t]=\int_0^t \lambda(\xi) d\xi$](img126.png)

-

![$ Var [N_t]=\int_0^t \lambda(\xi) d\xi$](img127.png)

Proof Recall that

![$\displaystyle E[N_t]=\left[\frac{dG_z(t)}{dz}\right]_{z=1}$](img128.png) and and![$\displaystyle \quad E[N_t^2]=\left[\frac{d^2G_z(t)}{dz^2}\right]_{z=1}+E[N_t]$](img129.png) |

|

From (8) we have

, and the two results

follow after immediate calculations.

, and the two results

follow after immediate calculations.

Theorem (Conditioning on the number of arrivals) Given that in the

interval the number of arrivals is , the arrival times

are independently distributed on with the pdf

.

.

Proof The proof of this theorem is analogous to that of the homogeneous

case. The probability of a single event happening at any of bins (Fig.

1) is given by

, where

, where  is the bin index. Given that exactly one event

occurred in the interval , we have

is the bin index. Given that exactly one event

occurred in the interval , we have

The argument for independence of two or more arrival times is identical to that

of the homogeneous case.

Question

What is the probability of observing events at instances

on the interval ?

Since arrival times

are continuous random variables,

the answer is 0. However, we can calculate the associated pdf as

Question How to generate a sample path of a point (Poisson)

process on ? It can be done in many different ways. For a homogeneous

process we use three methods:

- Conditioning on the number of arrivals. Draw the number of arrivals

from a Poisson distribution with parameter

, and then

draw numbers uniformly distributed on .

, and then

draw numbers uniformly distributed on .

- Method of infinitesimal increments. Partition the segment into

sufficiently small subsegments of length

(say

). For each subsegment draw a number

). For each subsegment draw a number  from a uniform distribution on

from a uniform distribution on ![$ [0,\,1]$](img139.png) . If

. If

, an event occurres in

that subsegment. We repeat the procedure for all subsegments. We can use the

approximation

, an event occurres in

that subsegment. We repeat the procedure for all subsegments. We can use the

approximation

for a less expensive procedure.

for a less expensive procedure.

- Method of interarrival times. Using the fact that inter-arrival times are

independent and exponentially distributed, we draw random variables

from exponential distribution with parameter , where

is the smallest integer that satisfies the criterion

from exponential distribution with parameter , where

is the smallest integer that satisfies the criterion

.

Then the sequence

.

Then the sequence

generates the required point process.

generates the required point process.

For an inhomogeneous process, the procedures 1 and 2 can be modified using

the appropriate theory of inhomegeneous Poisson process.

The illustration of the three procedures for a homogeneous case is given below.

We use  and

and

. For each different procedure

we generate

. For each different procedure

we generate  sample paths, and calculate the statistics by averaging over

ensemble. Raster plots of

sample paths, and calculate the statistics by averaging over

ensemble. Raster plots of  out of samples for the three methods

are shown in Fig. 6, Fig. 7 and Fig. 8,

respectively. Since the generated processes are homogeneous, the inter-arrival

time distribution is exponential with parameter . The histograms

of inter-arrival times corresponding to the three methods are also given below.

They clearly exhibit an exponenital trend. The sample mean and sample standard

deviation (unbiased) are also shown. Keep in mind that for exponentially

distributed random variables, both mean and standard deviation are given by

out of samples for the three methods

are shown in Fig. 6, Fig. 7 and Fig. 8,

respectively. Since the generated processes are homogeneous, the inter-arrival

time distribution is exponential with parameter . The histograms

of inter-arrival times corresponding to the three methods are also given below.

They clearly exhibit an exponenital trend. The sample mean and sample standard

deviation (unbiased) are also shown. Keep in mind that for exponentially

distributed random variables, both mean and standard deviation are given by

. Sample statistics indicates that is in the

vicinity of

. Sample statistics indicates that is in the

vicinity of  .

.

Figure 6:

Realization of a point process using conditioning on the number of

arrivals. (Top) Ten different sample paths of the same point process

shown as raster plots. (Bottom) The histogram of inter-arrival times, showing

the exponential trend

![\begin{figure}\centering\epsfig{file=rast_homo_1.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_1.eps, width=5.70in}\end{figure}](Timg151.png) |

Figure 7:

Realization of a point process using method of infinitesimal

increments. (Top) Ten different sample paths of the same point process

shown as raster plots. (Bottom) The histogram of inter-arrival times, showing

the exponential trend

![\begin{figure}\centering\epsfig{file=rast_homo_2.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_2.eps, width=5.70in}\end{figure}](Timg152.png) |

Figure 8:

Realization of a point process using method of independent

inter-arrival times. (Top) Ten different sample paths of the same point

process

shown as raster plots. (Bottom) The histogram of inter-arrival times, showing

the exponential trend

![\begin{figure}\centering\epsfig{file=rast_homo_3.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_3.eps, width=5.7in}\end{figure}](Timg153.png) |

Next: About this document ...

Up: Poisson Process, Spike Train

Previous: Poisson Process, Spike Train

Zoran Nenadic

2002-12-13

![$\displaystyle \mathbf{G}_X(z)=E[z^X]=\sum_{i=0}^{\infty}z^i p_i,

$](img36.png)

![\begin{displaymath}\begin{split}P(T_2>t,\,T_1\in(s-\delta,\,s+\delta]) &\le P(T_...

...(s-\delta,\,s+\delta])\,e^{-\lambda\,(t-2\,\delta)} \end{split}\end{displaymath}](img57.png)

![\begin{displaymath}\begin{split}P(N_{s-\delta}=0, \,N_{s+\delta}-N_{s-\delta}=1,...

...mbda\,t}&\le P(T_2>t,\,T_1\in(s-\delta,\,s+\delta]) \end{split}\end{displaymath}](img60.png)

![\begin{displaymath}\begin{split}&\left[\frac{d\mathbf{G}_t(z)}{dz}\right]_{z=1} ...

...a\,t\, e^{\lambda\,t(z-1)}\right]_{z=1}= \lambda\,t \end{split}\end{displaymath}](img68.png)

![\begin{displaymath}\begin{split}&\left[\frac{d^2\mathbf{G}_t(z)}{dz^2}\right]_{z...

...mbda\,t-(\lambda\,t)^2=\lambda\,t \quad\blacksquare \end{split}\end{displaymath}](img69.png)

![\begin{displaymath}\begin{split}&P(t_1\in(0,\,s],\,t_2\in(s,\,t])=P(N_s=1,\,N_t-...

..._s=1\vert N_s=1)=P(t_1\in(0,\,s])\,P(t_2\in(s,\,t]) \end{split}\end{displaymath}](img77.png)

![\begin{displaymath}\begin{split}R(t,s)&\triangleq E[N_t\,N_s]\\ R(t,s)&\overset{...

...lambda^2\,t^2+\lambda\,t=\lambda^2\,t\,s+\lambda\,t \end{split}\end{displaymath}](img98.png)

![$\displaystyle E[S_t]=\frac{d(\lambda t)}{dt}=\lambda$](img105.png)

![\begin{figure}\centering\epsfig{file=rast_homo_1.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_1.eps, width=5.70in}\end{figure}](img151.png)

![\begin{figure}\centering\epsfig{file=rast_homo_2.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_2.eps, width=5.70in}\end{figure}](img152.png)

![\begin{figure}\centering\epsfig{file=rast_homo_3.eps, width=5in} [0.1in]

\epsfig{file=hist_homo_3.eps, width=5.7in}\end{figure}](img153.png)